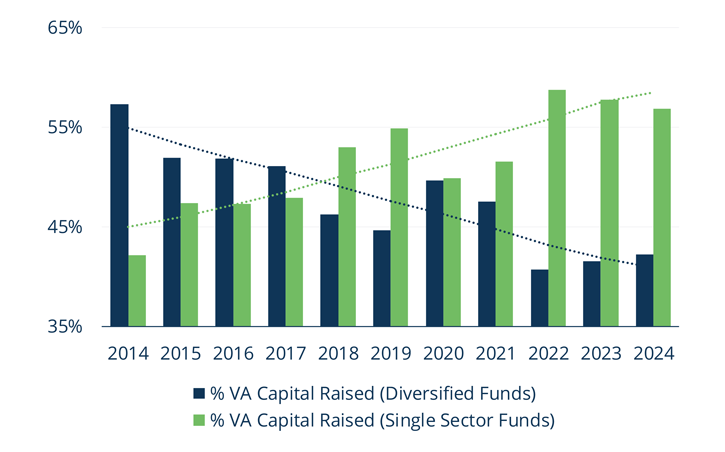

Seeking Value-Add Opportunities Today

In recent years, participants across the real estate market have been playing a waiting game. Buyers want to pick up quality assets at steep discounts, while owners don’t want to sell until asset values recover.

Blame the macroeconomic environment—high inflation prompted tightening monetary policy, namely higher interest rates, which weakened asset values, constrained liquidity and threw cold water on the investment sales market.

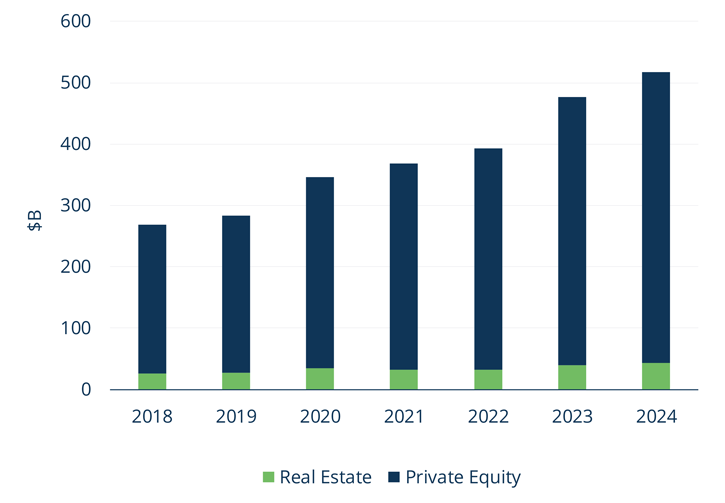

Yet, real estate secondaries have been a bright spot, showing remarkable growth following the Global Financial Crisis.

Appetite for bespoke liquidity solutions among general partners (GPs) continues to grow in the face of economic uncertainty and elevated interest rates because their investors are demanding liquidity and are also increasingly recognizing the portfolio benefits that secondaries can provide. Indeed, real estate secondaries fundraising reached over $4 billion per year on average from 2022-2024, which is more than double fundraising activity from $1.5 billion per year on average from 2008-2010.2

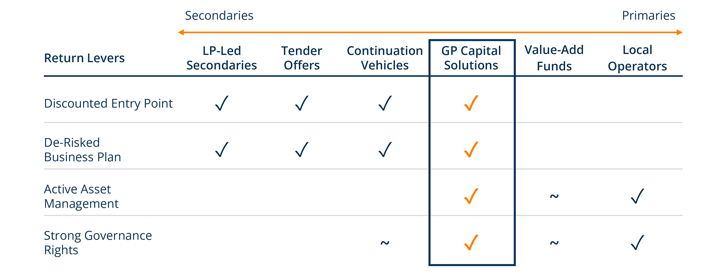

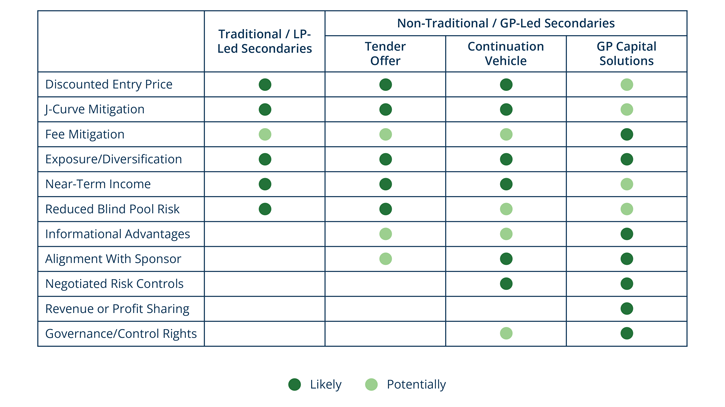

Real estate secondaries come in two main forms—limited partner (LP)-led and GP-led—and both offer benefits to investors. However, we believe that a specific type of GP-led secondary—known as GP capital solutions—is especially compelling today because it provides the opportunity to invest in high-quality, substantially de-risked real estate with the potential to generate value-add returns.

Here, we explore the broad landscape of real estate secondaries, including their potential investor benefits and risks, and provide insight into why we believe investors should consider adding GP capital solutions to their portfolios—provided they partner with managers who can add operational value.